Off-Balance-Sheet Financing Arrangements

Investors and lenders often use the proportion of debt in a firm’s capital structure as a measure of risk and therefore as a factor in establishing the cost of funds.16 Other things being equal, firms prefer to obtain funds without showing a liability on the balance sheet in the hope that future lenders or investors will ignore the risks associated with such financing. Firms sometimes structure innovative financing arrangements in ways that may not satisfy the criteria for the recognition of a liability, often transacting on situations where financial reporting treats the obligation (if any) as an executory contract or a contingency. The principal aim of such arrangements is to reduce the amount shown as liabilities on the balance sheet. Firms accomplish off-balance-sheet financing using a variety of approaches, including leases, the sale of receivables, product financing arrangements, use of another entity, use of joint ventures, and take-or-pay contracts

Leases

The most common and potentially largest source of off-balance-sheet financing is the use of operating leases However, at this point, it is useful to understand the effect of operating lease treatment on balance sheet quality. In a typical lease, lessors deliver a long-lived productive asset (delivery van, building, etc.) to a lessee in exchange for the lessee’s noncancelable promise to pay cash to the lessor over the lease term. Leases may be treated as operating or capital:

Investors and lenders often use the proportion of debt in a firm’s capital structure as a measure of risk and therefore as a factor in establishing the cost of funds.16 Other things being equal, firms prefer to obtain funds without showing a liability on the balance sheet in the hope that future lenders or investors will ignore the risks associated with such financing. Firms sometimes structure innovative financing arrangements in ways that may not satisfy the criteria for the recognition of a liability, often transacting on situations where financial reporting treats the obligation (if any) as an executory contract or a contingency. The principal aim of such arrangements is to reduce the amount shown as liabilities on the balance sheet. Firms accomplish off-balance-sheet financing using a variety of approaches, including leases, the sale of receivables, product financing arrangements, use of another entity, use of joint ventures, and take-or-pay contracts

Leases

The most common and potentially largest source of off-balance-sheet financing is the use of operating leases However, at this point, it is useful to understand the effect of operating lease treatment on balance sheet quality. In a typical lease, lessors deliver a long-lived productive asset (delivery van, building, etc.) to a lessee in exchange for the lessee’s noncancelable promise to pay cash to the lessor over the lease term. Leases may be treated as operating or capital:

- In an operating lease, the lessee does not record the asset received in property, plant, and equipment, and does not record the present value of the promised lease payments in long-term debt.

- Capital leases treat the transaction as the issuance of long-term debt to acquire a long-term asset.

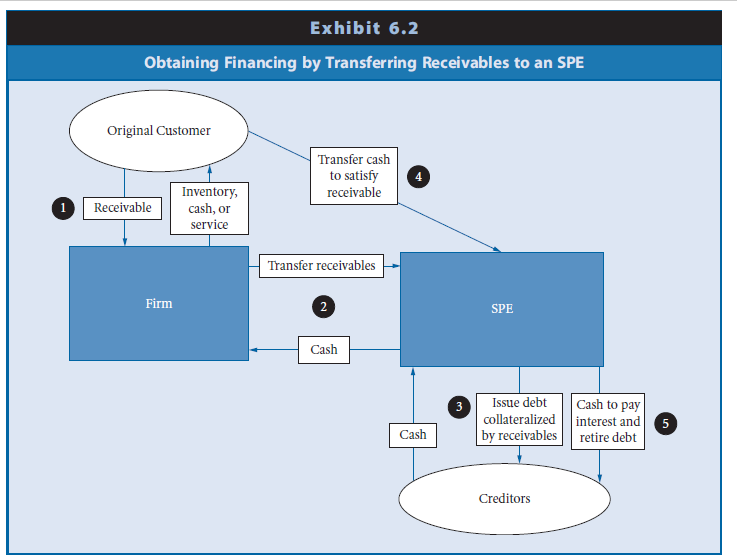

Sale of Receivables

Firms sometimes sell their receivables as a means of obtaining financing or use a special purpose entity (an SPE) to issue securities backed by the receivables (for example, mortgage-backed securities issued by financial institutions or their SPEs). Exhibit 6.2 illustrates the use of an SPE to accomplish the sale of receivables. In transaction 1, the firm sells inventory, lends cash, or provides services to an original customer. Rather than wait for customer payment, the firm transfers the receivables to the SPE in exchange for cash (transaction 2). The SPE obtains the cash it transfers to the firm from creditors by issuing debt (transaction 3). The debt is collateralized by the receivables. In transaction 4, the original customer pays off the receivables to the SPE, and in transaction 5, the SPE uses the cash to pay interest and principal to creditors. If collections from customers are not sufficient to repay the amount borrowed plus interest, the transferring firm may have to pay the difference; that is, the lender has recourse against the borrowing firm.

The question arises as to whether the recourse provision creates an accounting liability. Some argue that the arrangement is similar to a collateralized loan. The firm should leave the receivables on its books and recognize a liability in the amount of the cash received in transaction 2. Others argue that the firm has sold an asset; it should recognize a liability only if it is probable that collections from customers will be insufficient and the firm will be required to repay some portion of the amount received. The FASB and IASB provide accounting rules to guide the decision of whether to classify a transfer of receivables as a sale or a loan.19 For example, U.S. GAAP requires that firms recognize transfers of receivables as sales only if the transferor surrenders control of the receivables. Firms surrender control only if all of the following conditions are met:

- The assets transferred (that is, receivables) have been isolated from the selling (‘‘transferor’’) firm; that is, neither the transferor nor a creditor of the selling firm could access the receivables in the event of the seller’s bankruptcy.

- The buying (‘‘transferee’’) firm obtains the right to pledge or exchange the transferred assets, and no condition both constrains the transferee from taking advantage of its right and provides more than a trivial benefit to the transferor.

- The selling firm does not maintain effective control over the assets transferred through (a) an agreement that both entitles and obligates it to repurchase the assets or (b) the ability to unilaterally cause the transferee to return specific assets.

The principal refinement to the concept of an accounting liability is in identification of which party enjoys the economic benefits and sustains the economic risk of the assets (receivables in this case). If the selling (borrowing) firm controls the economic benefits/ risks, the transaction is a collateralized loan. If the arrangement transfers these benefits/ risks to the buying (lending) firm, the transaction is a sale.

Product Financing Arrangements

Product financing arrangements occur when a firm (sponsor) does either of the following:

- Sells inventory to another entity and, in a related transaction, agrees to repurchase the inventory at specified prices over specified times

- Arranges for another entity to purchase inventory items on the firm’s behalf and, in a related transaction, agrees to purchase the inventory items from the other entity

The first arrangement is similar to the sale of receivables with recourse except that greater certainty exists that the inventory transaction will require a future cash outflow. The second arrangement is structured to appear as a purchase commitment. In this case, however, the sponsoring firm usually creates an SPE for the sole purpose of acquiring the inventory. The sponsoring firm usually guarantees the debt incurred by the SPE in acquiring the inventory.

Exhibit 6.3 illustrates the use of an SPE to accomplish the product financing arrangement. In transaction 1, the SPE acquires inventory from a supplier by issuing a note payable. The firm also agrees to purchase the inventory from the SPE in the future, which is a purchase commitment (transaction 2). Because it is executory, the firm records neither the inventory nor the promise to pay for it. The firm generally guarantees the note or the SPE uses the purchase commitment as evidence of lower lending risk

The firm purchases the inventory from the SPE with cash (transaction 3) which is then

sent by the SPE to the supplier to pay off the note payable and interest. Financial reporting requires that firms recognize product financing arrangements as liabilities if they meet two conditions:

sent by the SPE to the supplier to pay off the note payable and interest. Financial reporting requires that firms recognize product financing arrangements as liabilities if they meet two conditions:

- The arrangement requires the sponsoring firm to purchase the inventory, substantiallyidentical inventory, or processed goods of which the inventory is acomponent at specified prices

- The payments made to the other entity cover all acquisition, holding, and financingcosts.

The second criterion requires that the sponsoring firm recognize a liability wheneverit incurs the economic risks (such as changing costs or interest rates) of purchasing and holding inventory, even though it may not physically control the inventory or have a legal obligation to the supplier of the inventory. Thus, as with sales of receivables with recourse, a firm recognizes a liability when it controls the determination of which party enjoys the economic benefits and incurs the economic risks of the asset involved. It alsorecognizes an asset of equal amount, usually inventory.

No comments:

Post a Comment