When the functional currency is the U.S. dollar, firms must use the monetary/nonmonetary translation method. The underlying premise of the monetary/nonmonetary method is that the translated amounts reflect amounts that the firm would have reported if it had originally made all measurements in U.S. dollars. To implement this underlying premise, it is necessary to distinguish between monetary items and nonmonetary items and translate each item at the appropriate exchange rate

- A monetary item is an account whose nominal maturity amount does not change as the exchange rate changes.

- From a U.S. dollar perspective, monetary items give rise to exchange gains and losses because the number of U.S. dollars required to settle the fixed foreign currency amounts fluctuates over time with exchange rate changes.

- Monetary items include cash, marketable securities, receivables, accounts payable, other accrued liabilities, and short-term and long-term debt.

- Firms translate monetary items using the end-of-the-period exchange rate and recognize translation gains and losses.

- These translation gains and losses increase or decrease net income each period whether or not the foreign unit must make an actual currency conversion to settle the monetary item. The rationale for the recognition of unrealized translation gains and losses in net income is that the foreign unit will likely make a currency conversion in the near future to settle monetary assets and liabilities or to convert foreign currency into U.S. dollars to remit a dividend to the parent. These activities are consistent with foreign units that operate as extensions of the U.S. parent.

- Nonmonetary items include inventories, fixed assets, common stock, revenues, and expenses.

- Firms translate nonmonetary items using the historical exchange rate in effect when the foreign unit initially made the measurements underlying these accounts.

• Inventories and cost of goods sold translate at the exchange rate when the foreign unit acquired

the inventory items.

• Fixed assets and depreciation expense translate at the exchange rate when the foreign unit acquired

the fixed assets.

• Most revenues and operating expenses other than cost of goods sold and depreciation translate at

the average exchange rate during the period.

• The objective is to state these accounts at their U.S. dollar-equivalent historical cost amounts. In this

way, the translated amounts reflect the U.S. dollar perspective that is appropriate when the U.S. dollar

is the functional currency

Illustration—U.S. Dollar Is Functional Currency

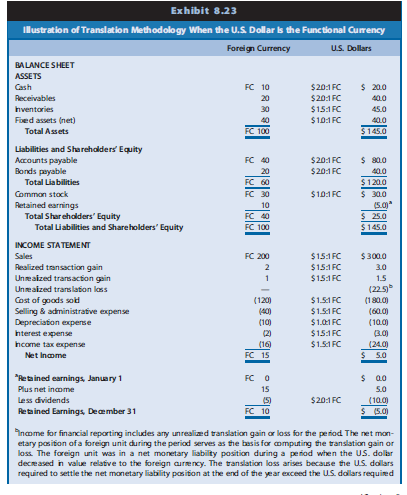

Exhibit 8.23 shows the application of the monetary/nonmonetary method to the data considered in Exhibit 8.22. Net income again includes both realized and unrealized transaction gains and losses. Net income under the monetary/nonmonetary translation method also includes a $22.5 translation loss.

As note (b) to Exhibit 8.23 shows, the firm was in a net monetary liability position during a period when the U.S. dollar decreased in value relative to the foreign currency. The translation loss arises because the U.S. dollars required to settle these foreigndenominated net liabilities at the end of the year exceed the U.S. dollar amount requiredto settle the net liability position before the exchange rate changed. The organizational structure and operating policies of a particular foreign unit determine its functional currency. The two acceptable choices and the corresponding translation methods were designed to capture the different economic and operational relationships between a parent and its foreign affiliates. However, firms have some latitude in deciding the functional currency (and therefore the translation method) for each

Illustration—U.S. Dollar Is Functional Currency

Exhibit 8.23 shows the application of the monetary/nonmonetary method to the data considered in Exhibit 8.22. Net income again includes both realized and unrealized transaction gains and losses. Net income under the monetary/nonmonetary translation method also includes a $22.5 translation loss.

As note (b) to Exhibit 8.23 shows, the firm was in a net monetary liability position during a period when the U.S. dollar decreased in value relative to the foreign currency. The translation loss arises because the U.S. dollars required to settle these foreigndenominated net liabilities at the end of the year exceed the U.S. dollar amount requiredto settle the net liability position before the exchange rate changed. The organizational structure and operating policies of a particular foreign unit determine its functional currency. The two acceptable choices and the corresponding translation methods were designed to capture the different economic and operational relationships between a parent and its foreign affiliates. However, firms have some latitude in deciding the functional currency (and therefore the translation method) for each

- Decentralize decision making to the foreign unit. The greater the degree of autonomy of the foreign unit, the more likely its currency will be the functional currency. The U.S. parent company can design effective control systems to monitor the activities of the foreign unit while permitting the foreign unit to operate with considerable freedom.

- Minimize remittances/dividends. The greater the degree of earnings retention by the foreign unit, the more likely its currency will be the functional currency. The parent may obtain cash from a foreign unit indirectly rather than directly through remittances or dividends. For example, a foreign unit with mixed signals about its functional currency might, through loans or transfer prices for goods or services, send cash to another foreign unit whose functional currency is clearly its own currency. This second foreign unit can then remit it to the parent. Other possibilities for inter-unit transactions are acceptable as well to ensure that some foreign currency rather than the U.S. dollar is the functional currency.

No comments:

Post a Comment